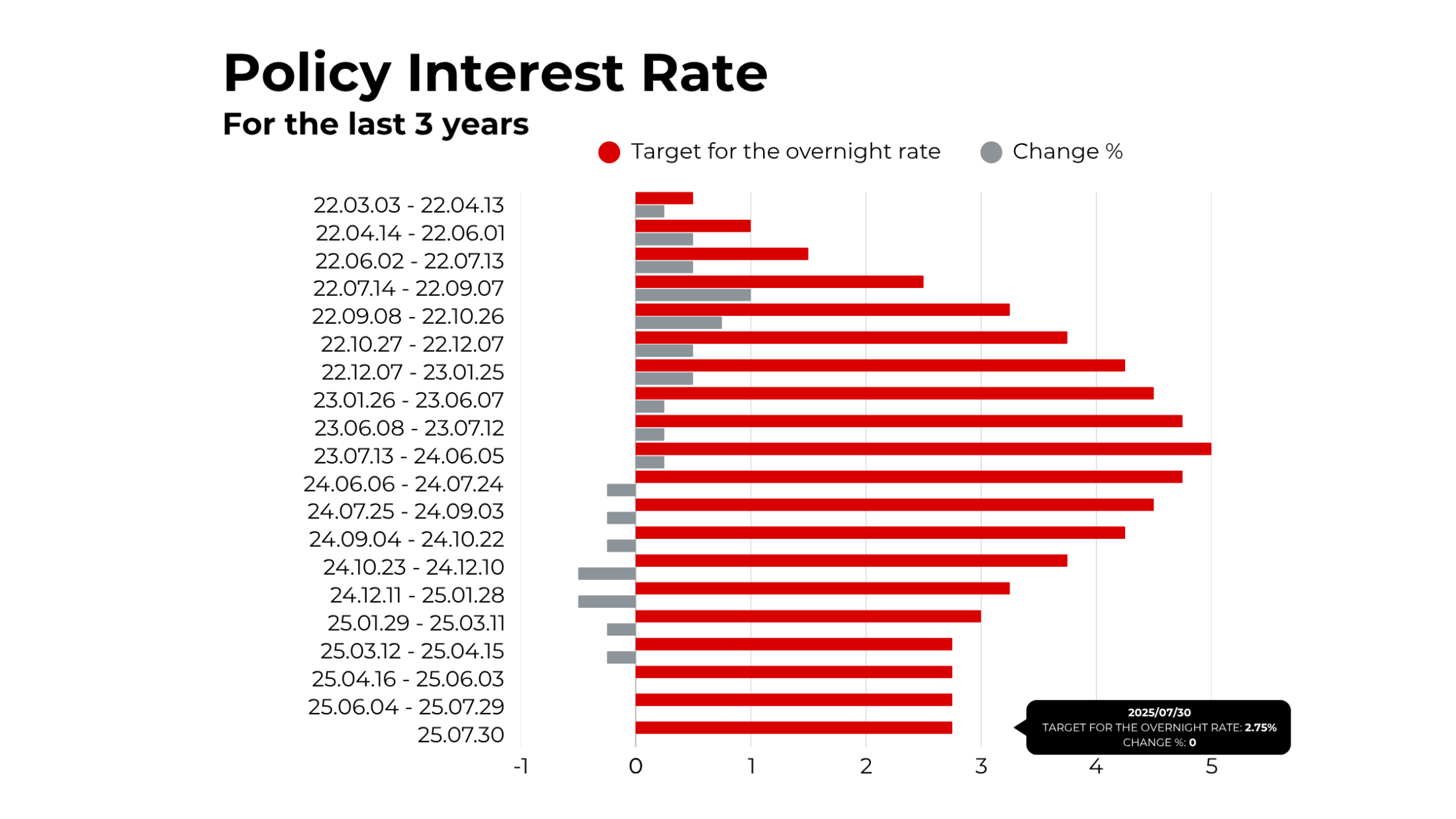

The Bank of Canada recently announced that they will be holding its key policy rate steady at 2.75%

Now, what does that actually mean for the real estate market and your next move?

💡 Quick Overview

The Bank of Canada decided not to change its interest rate. This key rate is the one that influences how much banks charge us on loans, mortgages, and lines of credit.

Right now:

Policy rate stays at 2.75%

Bank rate at 3%

Deposit rate at 2.70%

In simple terms, borrowing costs are holding steady for now.

🌍 What’s Behind the Decision?

Global trade tensions are still simmering, especially between the U.S. and other countries. Tariffs are making things unpredictable. These tensions affect everything from the cost of goods to how businesses operate, and even the strength of our own economy here in Canada.

Despite all this, Canada’s economy has shown some resilience. We had strong growth earlier this year, but that was partly due to businesses rushing to export goods ahead of new U.S. tariffs. After that rush, the economy slowed down a bit, GDP likely shrank by 1.5% in Q2.

And while unemployment is up slightly (6.9% in June) and wage growth is slowing, the overall picture isn’t all doom and gloom. Some sectors are still hanging in there.

🏘️ Why It Matters for Buyers and Sellers

If you're a buyer, this pause in interest rate changes is actually welcome news. It signals stability. Mortgage rates are closely tied to these decisions and with no hike this month, you're not seeing your future payments creep higher (at least for now).

If you're a seller, this stability helps buyer confidence. When borrowing costs are predictable, more people feel comfortable entering the market. That can help support demand for your property.

Plus, inflation is currently sitting around 2%, which means the Bank of Canada isn’t in a rush to cool the economy further unless something shifts.

What Could Happen Next?

The Bank is watching several moving parts closely:

Will U.S. tariffs slow our exports more?

Will uncertainty make businesses pull back on hiring or investing?

Will inflation heat up if companies pass on more of their cost increases?

If trade disruptions ease or the economy weakens further, there could even be a rate cut in the future. On the flip side, if inflation surprises on the upside, the Bank might have to tighten again.

What Should You Watch As a Buyer or Seller?

Mortgage rates: No change now, but keep your eye on fixed vs. variable trends.

Inflation: If inflation stays tame, pressure for rate hikes eases, this is a good news for affordability.

Economic confidence: The more stable things feel, the more active buyers and sellers become.

Global trade headlines: What’s happening in the U.S. and China might sound far away, but it has ripple effects here especially if it impacts jobs and costs.

📅 What’s Next?

The next Bank of Canada rate decision comes on September 17, 2025. That’s the date to circle if you’re watching the market or thinking of making a move.

We’re in a wait-and-see phase. Rates are holding steady, the economy is adjusting, and the real estate market is still finding its rhythm in this post-tariff, post-pandemic world. Whether you're buying your first home, upsizing, or planning to sell, it's a good time to stay informed and to keep asking the right questions.

If you ever want to talk through how all of this might affect your next step, we're always here to help interpret the bigger picture. But for now breathe easy, the rates are staying put.

Subscribe to our newsletter to stay posted on future rate updates.